Lee Shih and Peyton Teo summarise some key trends in judicial management in Malaysia.

Introduction

Judicial management (JM) is part of Malaysia’s corporate rescue mechanisms that came into force on 1 March 2018. Three years on, we set out the JM trends in our three-parter series of articles.

JM is a court-supervised rescue mechanism aimed at rehabilitating financially distressed companies. A court-appointed insolvency practitioner is empowered to manage the distressed company’s affairs, business and property. This insolvency practitioner is known as a judicial manager.

Once appointed, the judicial manager would prepare and table a statement of proposal for the creditors to vote on. The purpose of this is to either resuscitate the company and to continue as a going concern or alternatively, work towards a more advantageous realisation of the company’s assets than in a winding up for the benefit of its creditors.

The filing of a JM application triggers an automatic moratorium on all legal proceedings against the company. This gives breathing space to a financially distressed company to focus on its restructuring efforts to pivot back towards financial viability.

(1) Overall Judicial Management Trends

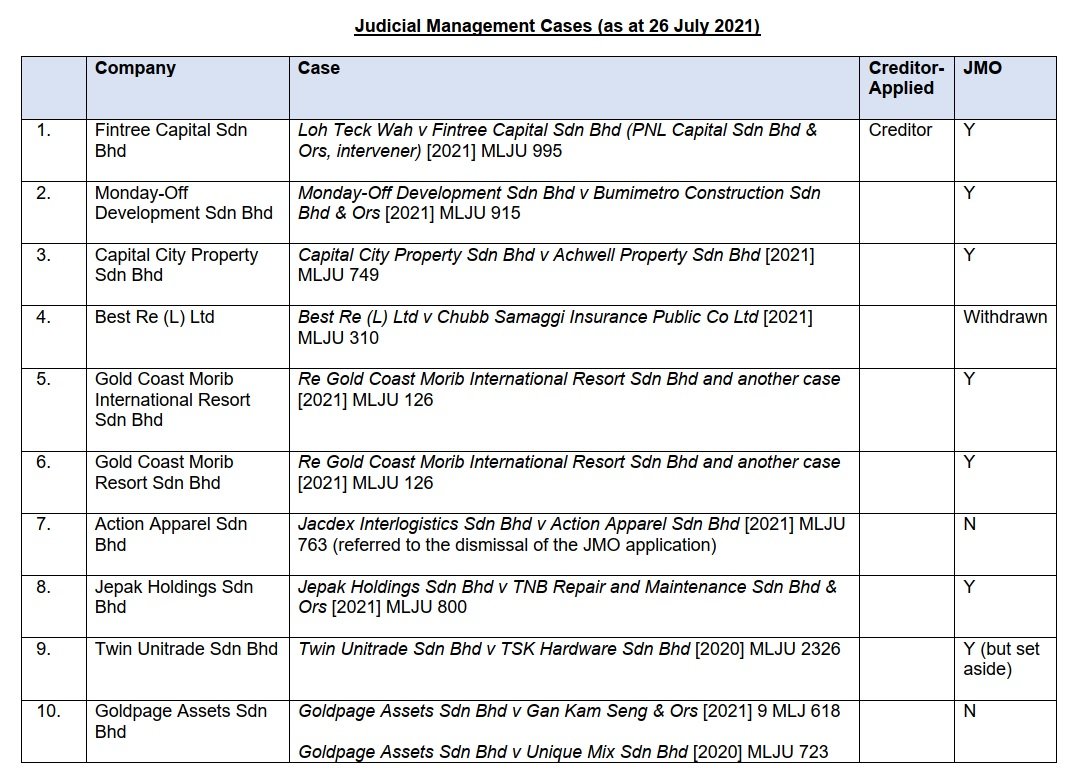

We looked at the reported judgments relating to JM. We found references to 20 companies that had applied for JM since the JM provisions came into force in March 2018.

The breakdown of the 20 companies is set out below with the case citations.

- 10 companies were placed in JM (but with 2 of those JM Orders subsequently set aside); and

- 8 companies had their JM applications dismissed

(2) Applicant: Debtor and Creditor

The vast majority of the 20 cases involve the applicant company itself applying for JM.

Nonetheless, 3 out of the 20 cases had creditors applying to place the debtor company into JM.

Section 405 of the CA 2016 allows for “a creditor, including any contingent or prospective creditor” to make the application for JM. Section 405 itself does not define the term “contingent or prospective creditor”.

The High Court has taken a broad reading of the term “creditor”.

In Spacious Glory Sdn Bhd v Coconut Three Sdn Bhd [2020] MLJU 1827 (grounds of judgment), the Court found that the party claiming to be a creditor did have standing to apply for JM.

The Court held that the phrase “contingent or prospective creditor” will denote where the company may become subject to a present liability on the happening of some future event or at some future event. The term “creditor” must include all persons having any pecuniary claims against the company.

Spacious Glory was applied in Loh Teck Wah v Fintree Capital Sdn Bhd [2021] MLJU 995 (grounds of judgment). In this case, the Court also decided that the applicant-creditor did have standing to apply for JM. The applicant had demonstrated on a balance of probabilities that he was a creditor and therefore could apply to place Fintree Capital into judicial management.

(3) Labuan Company

A Labuan company would not be able to apply for JM. A Labuan company is incorporated under the Labuan Companies Act 1990 (LCA) and where the CA 2016 corporate rescue mechanism does not extend to the LCA.

Nonetheless, in Best Re (L) Ltd v Chubb Samaggi Insurance Public Co Ltd [2021] MLJU 310 (grounds of judgment dated 9 February 2021), a Labuan company filed for an application for JM on the eve of the hearing of a winding up petition filed against the Labuan company. The petitioning creditor was allowed to intervene in the JM proceedings.

From reading the court papers filed, the Labuan company subsequently withdrew the application for JM. The creditors who intervened in the JM application raised the legal point that a Labuan company could not apply the JM provisions under the CA 2016.

(4) Public Listed Company

It remains untested whether a public listed company can apply for JM.

Section 403(b) of the CA 2016 excludes from JM “a company which is subject to the Capital Markets and Services Act 2007.” It is a broad reference and with no judicial interpretation of this phrase.

The listed company, Scomi Group Bhd, has filed an application for JM (more on this over here). The creditors who have intervened in the application have raised the issue that a listed company would fall within that phrase of a company subject to the Capital Markets and Services Act 2007. We look forward to seeing the Court’s determination of this issue.

In the future, the proposed amendments to the CA 2016 will allow public listed companies to apply for judicial management. Section 403(b) of the CA 2016 will be replaced with the exception of “a company which is approved or licenced by SC under the CMSA 2007 or Securities Industry (Central Depositories) Act 1991 (SICDA 1991) or prescribed upon the written request by Ministry of Finance (MOF).” Therefore, only these particular licensed entities will be excluded from applying for JM.

(5) Full and Frank Disclosure on Ex Parte Application for JM

There are cases that have now decided that there must be full and frank disclosure when making the application for JM. This is because filing the application is treated as akin to a without notice application.

In the first judicial management case of Leadmont Development Sdn Bhd v Infra Segi Sdn Bhd [2019[ 8 MLJ 473 (the case update can be found here), the High Court emphasised the applicant’s duty to make full and frank disclosure when applying for the JM Order. This is especially where in that case, the JM Order was essentially an ex parte Order since no creditors appeared at the hearing.

In Twin Unitrade Sdn Bhd v TSK Hardware Sdn Bhd [2020] MLJU 2326 (grounds of judgment dated 30 December 2020), the High Court found there was a failure to make full and frank disclosure of all material facts at the time of the application for JM. The Court set aside the JM Order.

In Vision Development Concept Sdn Bhd v Low Sheh Ling [2020] MLJU 2387, the duty of full and frank disclosure was strict. By the time of the hearing of the application for JM, other creditors had intervened. Hence, it was a contested inter partes hearing.

Nonetheless, the Court was unimpressed that the applicant company had not fully disclosed all matters at the time it filed the application. The issues were only addressed after the creditors had raised their contentions. Therefore, the Court viewed the application as not entirely bona fide and that the applicant had withheld material information and facts from the Court.

In Part 2, we will cover other emerging trends like the interim judicial manager, the need for the proposed judicial manager’s affidavit, the public interest consideration, and other issues.

Peyton Teo is currently a paralegal with Lim Chee Wee Partnership. She is a law graduate and is currently waiting for her CLP results.

The full series of judicial management trends after three years: